NOTE: Aviva MyLifeIncome II has been phased out and replaced by Singlife Flexi Life Income II.

Aviva MyLifeIncome II is a sustainable, supplementary income plan that gives you a lifetime of yearly payouts, with 100% principal guaranteed feature. You can start to receive a lifetime of yearly income, as short as 5 years after placing a single premium for all your life purposes.

Alternatively, choose to accumulate your yearly income for higher financial gains until you need the money for even bigger life goals and objectives.

Aviva MyLifeIncome II product details

Aviva MyLifeIncome II is featured for Cashback benefits in our 4 Best Regular Insurance Savings Plans in Singapore (Updated)

Aviva MyLifeIncome II is featured for Flexibility of Withdrawing Capital benefits in our 4 Best Insurance Plans for Retirement Income (Updated)

- Life policy – Annuity

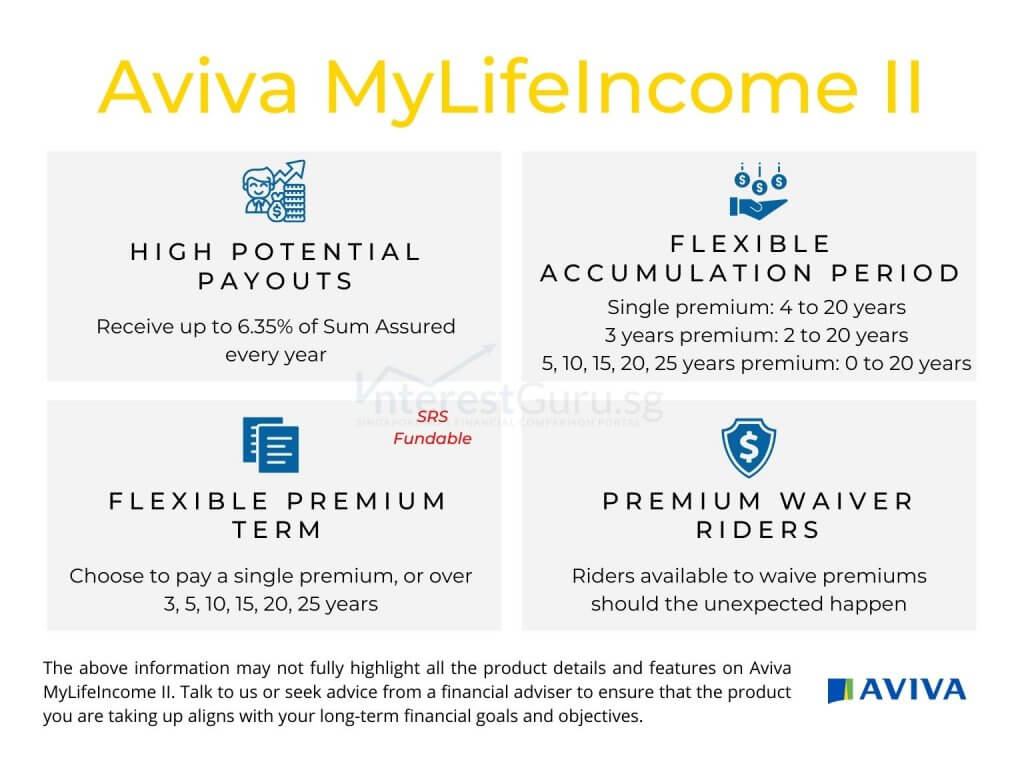

- Built-in Death and Terminal Illness coverage

- Flexible Premium Term

- Choose to pay a single lump-sum premium or over 3, 5, 10, 15, 20 or 25 years

- Choose to pay premiums by cash or Supplementary Retirement Scheme (SRS)

- Accumulation period options (Based on premium payment term) up to 80 years of age:

- For Single Premium: 4 to 20 years

- For 3 years premium payment term: 2 to 20 years

- For 5, 10, 15, 20, 25 years premium payment term: 0 to 20 years

- High payouts of up to 6.35% of Sum Assured every year

- Guaranteed Lifetime Yearly Income = Guaranteed Cash Benefit 0.95% of Sum Assured) on top of any Non-guaranteed Cash Bonus (5.4% of Sum Assured)

- 100% Capital Guaranteed

- At the end of the accumulation period or earlier, depending on your chosen premium payment term

- Wide range of Premium waiver riders to waive premiums for insurable events

- Cancer Premium Waiver II

- Future premiums waived in the

event policyholder is diagnosed with

Major Cancer

- Future premiums waived in the

- EasyTerm

- Lump-sum cash payment of up to five

times basic plan’s annual premium

in the event of policyholder’s Death,

Terminal Illness or Total and

Permanent Disability.

- Lump-sum cash payment of up to five

- EasyPayer Premium Waiver

- Future premiums waived in the

event of policyholder’s Death, Terminal

Illness or Total and Permanent Disability

- Future premiums waived in the

- Cancer Premium Waiver II

- Booster Bonus

- Receive additional non-guaranteed 0.5% of Sum Assured every year

- You can choose to reinvest the yearly payouts and booster bonus at the prevailing non-guaranteed rates

- Enjoy hassle-free application with no health questions asked

Aviva My Life Income II is a common search alternative for Aviva MyLifeIncome II

Read about: 4 Best Retirement Plans and Annuity Policies in Singapore (Updated)

Features of Aviva MyLifeIncome II at a glance

Cash and Cash Withdrawal Benefits

Cash value: Yes

Cash withdrawal benefits: Yes

Health and Insurance Coverage

Death: Yes

Total Permanent Disability: Yes

Terminal Illness: Yes

Critical Illness: N.A

Early Critical Illness: N.A

Health and Insurance Coverage Multiplier

Death: N.A

Total Permanent Disability: N.A

Terminal Illness: N.A

Critical Illness: N.A

Early Critical Illness: N.A

Optional Add-on Riders

EasyTerm

Cancer Premium Waiver

EasyPayer Premium Waiver

Additional Features and Benefits

Yes.

For further information and details, fill up the form below and let us advise accordingly.

Read about: How can I accumulate a million dollar (Realistically)

Read about: The Complete Guide to Retirement Planning in Singapore (Updated)

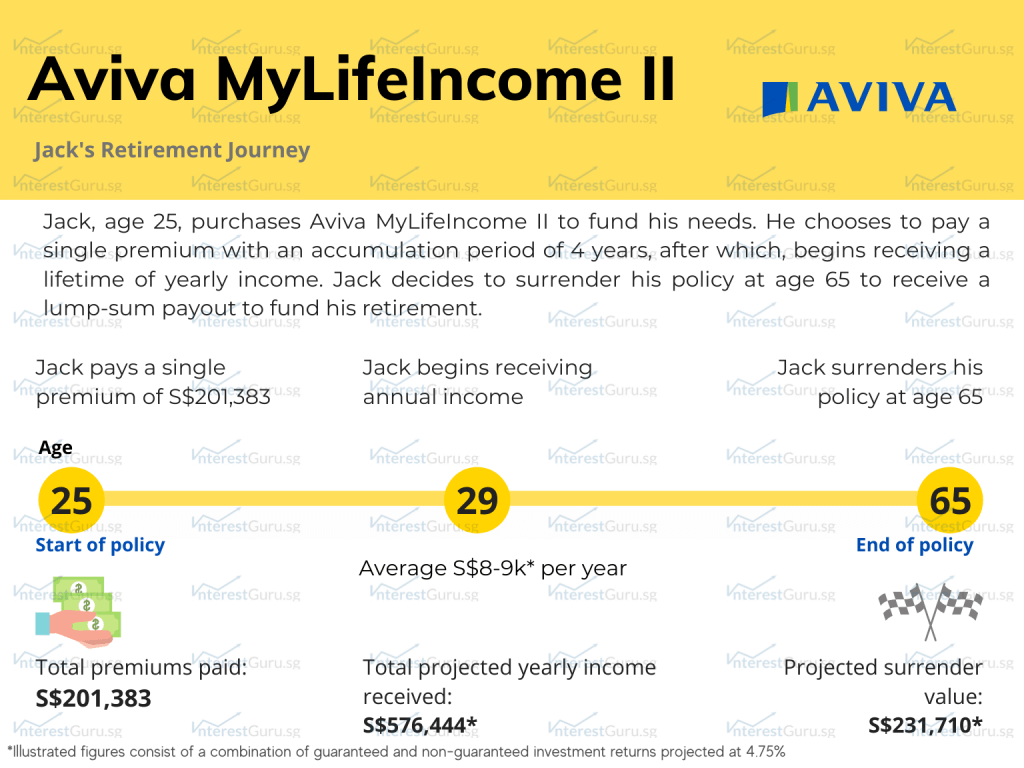

Policy Illustration for Aviva MyLifeIncome II, Jack

Jack, 25 years old, purchases Aviva MyLifeIncome II for his retirement. He chooses to pay a single premium of S$201,383 with an accumulation period of 4 years.

From the 5th policy year onwards, Jack starts receiving a projected yearly income of S$8,699 consisting of guaranteed income on top of non-guaranteed bonuses. That sum increases to S$9,384 when Jack turns 60.

By age 65, Jack would have received a total of S$576,444 in projected yearly payouts. He decides to surrender his Aviva MyLifeIncome II policy to receive a projected lump-sum surrender payout of S$231,710 to spend as he wishes.

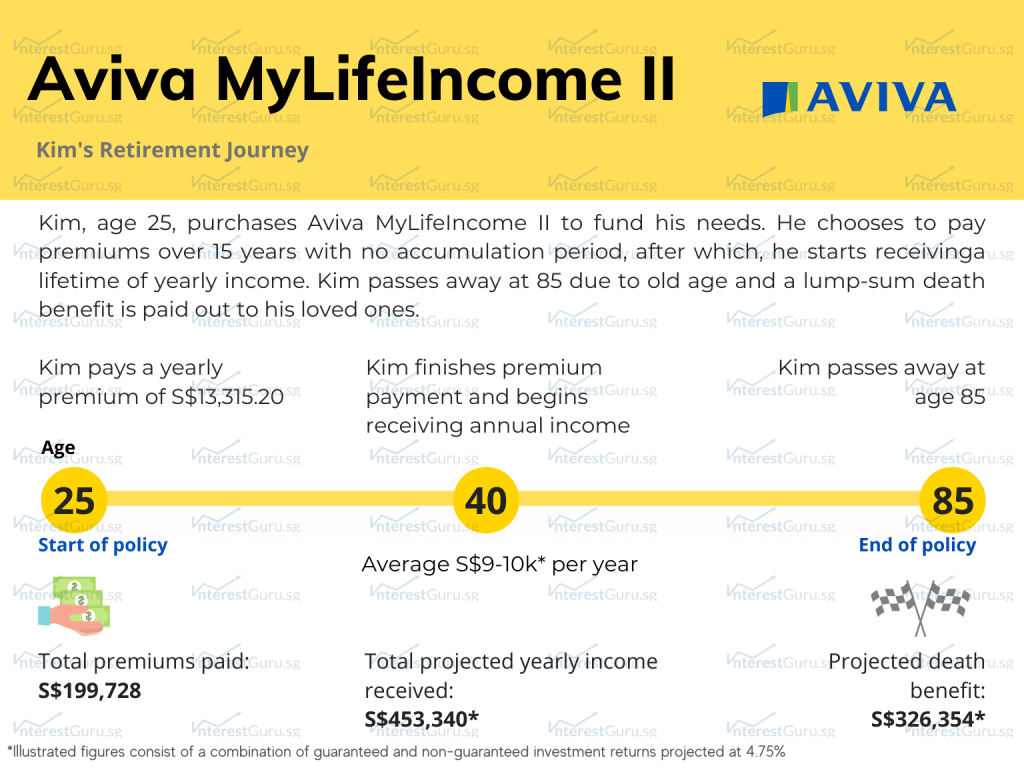

Policy Illustration for Aviva MyLifeIncome II, Kim

Kim, 25 years old, purchases Aviva MyLifeIncome II for his retirement. He chooses to pay a yearly premium of S$13,315.20 for the next 15 years with no accumulation period.

By age 40, with a total of S$199,728 in premiums paid, Kim starts receiving a total projected yearly income of S$9,652 consisting of guaranteed income on top of non-guaranteed bonuses until age 60 where his yearly income increases to S$10,412.

By age 85, Kim would have received a total of S$453,340 in total projected yearly payouts. However, Kim passes away shortly after his 85th birthday. His loved ones are set to receive a projected lump-sum death benefit of S$326,354.

Aviva MyLifeIncome II may be suitable if you are looking for

Aviva MyLifeIncome II may potentially be a good fit if the following matters to you:

- Regular cash payout upon your desired retirement age

- Saving regularly over a period of time or

- Single lump-sum premium with no future financial commitments

- Insurance options without medical underwriting

- To potentially generate higher financial returns compared to bank accounts

- Insurance policy with a high surrender value in the early years of the policy

Read about: When should you start making plans for retirement?

Read about: The effects of compounding returns on your savings

Aviva MyLifeIncome II may not be suitable if you are looking for

Aviva MyLifeIncome II may potentially be a bad fit if the following matters to you:

- Health and Protection coverage

- High insurance coverage for Death or Terminal Illness

- High insurance coverage for Early Critical Illness, Critical Illness or Total Permanent Disability

- Potentially higher financial returns compared to a pure investment product.

Read about: Why should you choose a shorter premium term on your insurance policies

Further considerations on Aviva MyLifeIncome II

- How is Aviva or Aviva MyLifeIncome II investment returns based on historical performance?

- How does Aviva MyLifeIncome II compare with retirement plans and annuity policies from other insurance companies?

- Can Aviva MyLifeIncome II fulfill my financial, insurance, health, and protection needs?

The above information may not fully highlight all the product details and features on Aviva MyLifeIncome II. Talk to us or seek advice from a financial adviser before making any decision about Aviva MyLifeIncome II.

Always ensure your long-term financial goals and objectives are aligned with the financial product you are considering to take up.

Read about: 4 Best Retirement plans and Annuity Policies in Singapore (Updated)

Is Aviva MyLifeIncome II suitable for me?